The Centers for Medicare & Medicaid Services (CMS) recently issued Advisory Opinion No. CMS-AO-2021-01, clarifying that physician groups that furnish designated health services (e.g., laboratory, imaging) through wholly-owned subsidiary physician practices that are separately enrolled in Medicare and commercial payors but do not, themselves, qualify as group practices under the federal physician-self referral law (commonly referred to as the “Stark Law” or “Stark”), can qualify as a group practice as defined by Stark. Specifically, CMS stated that, based on the particular facts, the physician practice requestor (Group Practice) would not be precluded from complying with the “single legal entity” requirement for a group practice under Stark if designated health services were provided to Medicare beneficiaries through such wholly-owned subsidiary physician practices where the Group Practice employs or contracts with all clinical employees and all revenues and expenses of the subsidiaries are treated as revenues and expenses of the Group Practice.

Single Legal Entity Requirement for Group Practices

Stark prohibits a physician from making referrals for certain designated health services payable by Medicare to an entity with which such physician (or an immediate family member thereof) has a financial relationship, unless an exception applies.[1] One such exception – the exception for in-office ancillary services[2] – is available to a physician practice with multiple physicians if it qualifies as a “group practice” as defined at 42 C.F.R. § 411.352. A qualifying group practice must “consist of a single legal entity operating primarily for the purpose of being a physician group practice in any organizational form recognized by the State in which the group practice achieves its legal status . . .” (emphasis added).[3]

CMS discussed the single legal entity requirement for group practice structures in an August 1995 final rule[4] (1995 Rule), providing that a group practice could not “consist of two or more groups of physicians, each organized as separate legal entities.” But, the single legal entity requirement would not preclude a single group practice from owning other legal entities for the purpose of providing services to the group practice. A 2001 final rule (2001 Rule) added that physicians are members of a group practice during the time that they furnish “patient care services” to patients of the group for the benefit of the group, even if such services (e.g., administrative services) are not billable by the group.[5]

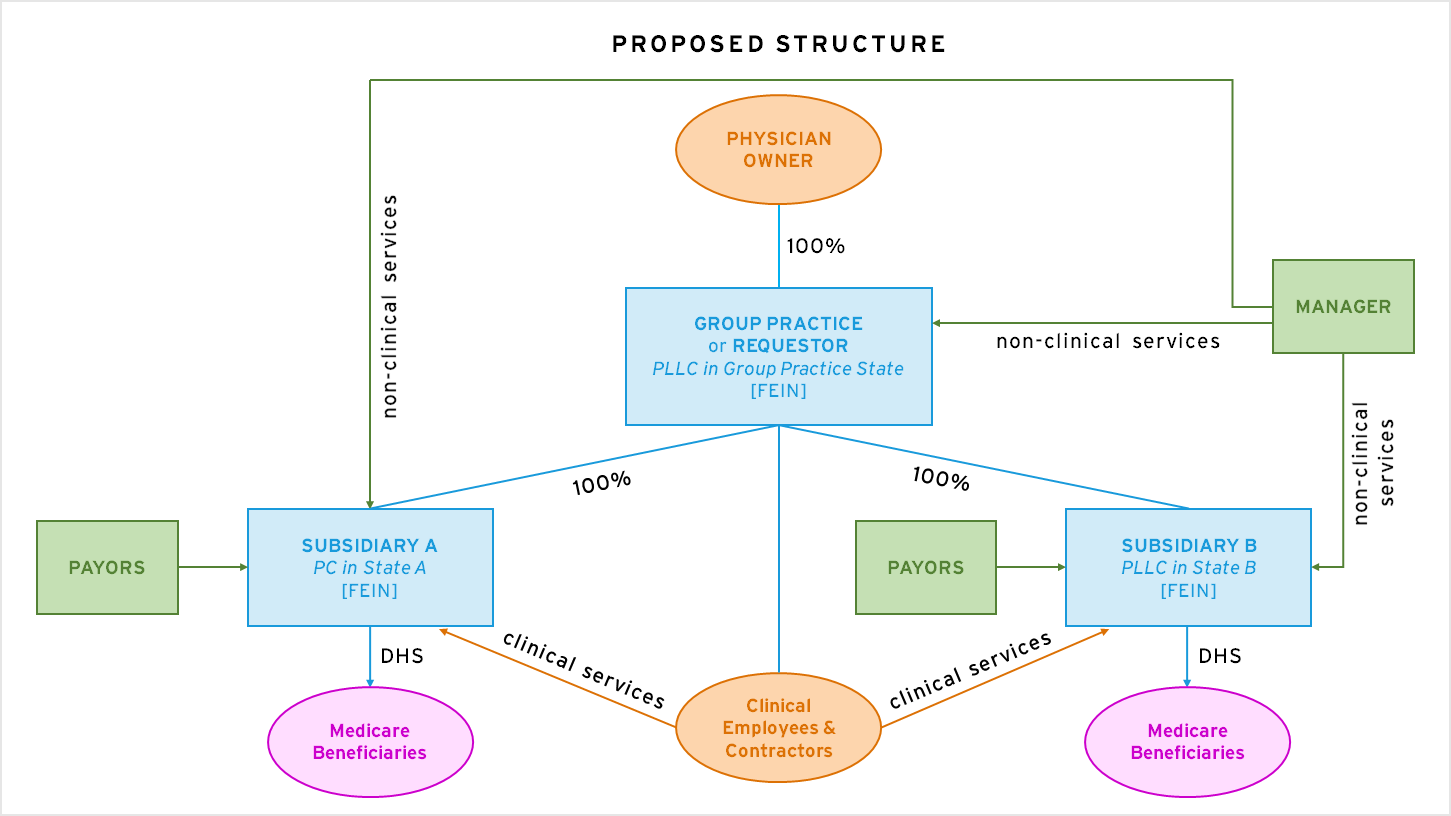

Proposed Group Practice Structure

Group Practice requested an advisory opinion in the context of a proposed acquisition of two physician practices under common ownership by the same physician owner (Subsidiary A and Subsidiary B). Group Practice asked whether it would fail to qualify as a group practice under Stark if, following the proposed acquisition, Subsidiary A and Subsidiary B furnished designated health services to Medicare beneficiaries, but the subsidiaries themselves did not qualify as group practices under Stark. In its request for an advisory opinion, Group Practice certified that it satisfied all other requirements of Stark’s group practice definition, including that it is a unified business with centralized decision making.

In the proposed structure, Group Practice would remain under the ownership of its physician owner and would acquire the equity of Subsidiary A and Subsidiary B such that the entities would become wholly-owned subsidiaries of Group Practice. Meanwhile, all of the material assets and business functions of the subsidiaries would be transferred to Group Practice or the management company. Patients of the subsidiaries would be considered patients of Group Practice. Subsidiary A and Subsidiary B would provide designated health services to patients (including Medicare beneficiaries) at their respective office sites under the supervision of clinical personnel employed or contracted by Group Practice. The subsidiaries would maintain their respective payor arrangements and bill government and commercial payors for medical services furnished, including designated health services, and all revenues and expenses of the subsidiaries would be treated as the revenues and expenses of Group Practice.

Based on these facts, CMS concluded that Group Practice would not be precluded from complying with the single legal entity requirement for group practices seeking to meet the in-office ancillary services exception under Stark if designated health services were furnished through a wholly-owned subsidiary physician practice that does not itself qualify as a group practice under Stark. CMS appeared to rely, in part, on the following aspects of the proposed group practice structure when issuing its favorable determination:

- All revenues and expenses of Subsidiary A and Subsidiary B would be treated as the revenues and expenses of Group Practice, although Subsidiary A and Subsidiary B would maintain their separate Medicare enrollments and payor contracts and bill under their own billing numbers.

- The designated health services provided at the subsidiary level would be furnished or supervised by clinical personnel employed or contracted directly by Group Practice.

CMS did not opine on Group Practice’s compliance with group practice requirements beyond the single legal entity requirement if it were to consummate the proposed acquisition or whether the provision of designated health services through Subsidiary A or Subsidiary B would satisfy the requirements of the exception for in-office ancillary services under Stark. CMS’s analysis of the proposed group practice structure gives providers welcomed flexibility and clarity for structuring group practice arrangements involving wholly-owned subsidiary physician practices.

For more information about updates to the Stark group practice regulations, among other regulations, taking effect on January 1, 2022, see our analysis at this link. If you have any questions about group practice structures under Stark, please contact the authors.

2 See 42 C.F.R. § 411.350 et seq.